Direct Consumer Deposit Account Agreement

Last updated: July 29, 2024

Please read this Direct Deposit Account Agreement (the “Agreement”) carefully and retain it for your future reference. This Agreement contains the general terms, conditions and disclosures related to the demand deposit account (the “Account”) issued by Pacific West Bank, a bank chartered under the laws of the State of Oregon (the “Bank”), a member of the Federal Deposit Insurance Corporation (FDIC). Direct, Inc (“Program Partner”) is responsible for managing the Account program on behalf of Bank.

When you see the words “we,” “us,” or “our” in this Agreement, it refers to the Bank any of the Bank’s affiliates, successors, or assignees. When you see the words “you” or “your,” it refers to the individual who opens an Account and in whose name an Account is maintained on our records, and any joint owner of each Account.

By opening and continuing to hold an account with us, you agree to be bound by this Agreement.

IMPORTANT NOTE: THIS AGREEMENT IS SUBJECT TO BINDING ARBITRATION AND A WAIVER OF CLASS ACTIONS AND YOUR RIGHT TO A JURY. THE TERMS OF ARBITRATION AND THE WAIVER APPEAR IN THE SECTION OF THIS AGREEMENT TITLED “ARBITRATION AND WAIVERS” BELOW.

1 Account Overview

1.1 How to Contact Us

You may contact us with any questions or concerns regarding your Account, including to access your statements and transaction history. All communication between you and us will be handled by the Program Partner.

The best way to contact us is through email at ClientService@DirectB.net. You may also contact us by telephone at 1-503-344-1230.

1.2 Type of Account and Eligibility

The Account is a non-interest-bearing demand deposit account used to hold your deposits and make certain types of payments and transfers. When we receive the funds that you deposit to your Account, the funds will be held and accounted for so as to be insured by the FDIC, subject to applicable limitations and restrictions of such insurance. To open an Account, you must be a United States citizen or lawful permanent resident, have a physical address within the fifty (50) United States, the District of Columbia or a military address (APO or FPO), be at least 18 years of age, and have a valid Social Security Number. Other eligibility requirements may apply. This Account is only available to individuals for personal, family or household purposes and may not be opened by a business in any form or used for business purposes.

We may set such eligibility criteria or decline to open an Account for any reason permitted by law and at our sole discretion. We are not liable for any Losses (as defined below) resulting from refusal of an Account relationship. We may also limit the number of Accounts that you have in our sole discretion. Your Account is subject to security and fraud prevention restrictions at any time, with or without notice.

1.2.1 Account Types

We offer two (2) types of Accounts: Classic and Home Rewards.

The Classic Account is the default Account designation for non-mortgage users.

You may be eligible for a Home Rewards Account if you maintain a minimum balance of $5000.00 in your DIRECT account beginning no less than 30 days after account opening OR have a minimum of 10 completed purchases with your DIRECT debit card, refunds do not apply. See DIRECT Home Rewards agreement for more information regarding the mortgage user.

The Account that you are placed in may affect your fees as set forth in this Agreement. Unless otherwise stated in this Agreement, all terms contained in this Agreement apply equally to both Accounts.

1.3 Online or Mobile Access To Your Account

When you open an Account, you may also be enrolled in an online business banking service or mobile application (collectively, “Online Banking Services”) offered by the Program Partner that you can use to access your Account, view information about your Account and conduct certain transactions. You may also be given access to various features through the Online Banking Services separate from your Account. If you cancel your enrollment in the Online Banking Services at any time, we may close your Account as detailed below.

Unless otherwise specified in this Agreement, the Online Banking Services and its features are governed by the Program Partner’s additional terms of service and other agreements, as well as the Program Partner’s privacy policy, which may be provided to you separately or made available through the Program Partner’s website. Please review these documents carefully because by using the Online Banking Services, you agree to be bound by them. These services are not provided or controlled by the Bank or this Agreement.

1.4 Paperless Account

To open an Account, you must agree to go “paperless.” This means that you must (a) provide us with and continue to maintain a valid email address and (b) accept electronic delivery of all communications that we need or decide to send you in connection with your Account by agreeing to the Program Partner’s ESIGN Consent Agreement.

1.5 Joint Accounts

We and the Program Partner may, in our respective discretion, allow for the joint ownership of accounts. Such “Joint Accounts” are owned by two people and all deposits made into the accounts are owned by both people. Such joint Accounts are not community property and are not held as tenants in common. Funds in joint Accounts are payable to or at the direction of any accountholder (regardless of who contributed the funds and the amount of contributions). For all Accounts, except for certain retirement benefits like Social Security, if one person dies, the money in the Account then belongs only to the survivor and not to the estate of the deceased person. The owners of the Account are considered “joint tenants” with right of survivorship. Any owner of the Account may: (a) tell us to pay a person or company; (b) withdraw, transfer funds or close the Account without the other owner's consent; (c) pledge the Account to us as collateral for a debt owed to us; and/or (d) deposit checks payable to any joint owner. Each of you can enter a stop payment order on any payments or other orders of withdrawal authorized by either of you. Your liability as an owner of a joint Account is joint and several. This means that we can enforce this Agreement against, as well as seek repayment of any amount owed from, any one of you, some of you, or all of you, including for any overdrafts.

If one joint owner requests that we not pay items authorized by a different joint owner, we may restrict the Account and refuse to pay all items (including items authorized by the owner making the request), but we are not required to do so. If we restrict the Account, we may not release the restriction unless all joint owners agree in writing to remove it. No request to restrict the Account will affect items that we paid before the request. If we decide not to restrict the Account, all joint owners remain responsible for items subtracted from the Account. We may also pay all or any part of the funds in the Account to a court or government agency if we receive a garnishment, levy or similar legal process that identifies any of the joint owners.

1.6 Authorized Users

You may be given the ability to designate individuals (“Authorized Users”) who you authorize to access your Account and/or conduct transactions through your Account, and such designation right includes the responsibility to determine the scope of rights and capabilities that the individual will have with respect to your Account. When you have consented to adding an Authorized User, you understand that any transaction authorization, instruction or any other action concerning your Account that your Authorized User engages in will be deemed authorized by you and valid and we are under no obligation to investigate the authorization, instruction or activity. You also agree that you will not hold us liable for acting upon any such authorization, instruction or activity. We reserve the right to terminate your Authorized User’s access to the Account for any reason and without advance notice.

We will continue to treat all actions taken by your Authorized User as authorized by you until you revoke the Authorized User’s access to your Account by notifying us as listed above or through the Online Banking Services, as available. Until we have been properly notified in writing of any change in such authorization and we have had a reasonable period of time to act upon such notice, we may pay, apply, or otherwise honor and charge your Account, without inquiry, without limit as to amount, and without regard to the application of the proceeds thereof all orders for payment or transfer of money for whatever purpose. You must notify us immediately as specified above of any change in the status of any Authorized User. We may ask you to give us additional documentation. No action taken by us before we receive proper notification in writing of any such change and have had a reasonable period of time to act upon such notice will be affected by any such notice.

1.7 How To Open an Account

You may open an Account by visiting the Program Partner’s website at www.directb.net and following the instructions there.

You may also open an Account by downloading the DIRECT mobile application and following the instructions within the application.

Each person completing the Account opening process or otherwise completing any Account opening requirements represents and warrants that he, she or they:

● Are authorized to execute all documents or otherwise complete our requirements in his, her or their stated capacity;

● Have furnished all documents or other information necessary to demonstrate that authority;

● Will furnish other documents and complete other requirements as we may request of him, her, or them;

● Certify that, to the best of his, her or their knowledge, all information provided to us is complete and correct; and

● he, she, or they have read this Agreement and agree to be bound by and comply with its terms.

We may refuse to recognize any document affecting the Account that appears to us to be incomplete, improperly executed, or fraudulent.

Important information about procedures for opening a new Account: To help the government fight the funding of terrorism and money laundering activities, federal law requires all financial institutions to obtain, verify and record information identifying each person who opens an Account, including any Authorized Users who may access an Account. This means that when you open an Account, we will ask for information that allows us to identify you, including your name, legal address, Social Security Number or Tax Identification Number, date of birth and other information that will allow us to identify you. We also may ask for a driver’s license or other identifying documents for Authorized Users, account owners, and others.

1.8 Minimum Deposits and Balances

To maintain eligibility for your Home Rewards account, you must either:

· Maintain a minimum balance of $5000.00 in your DIRECT account beginning no less than 30 days after account opening: OR

· Have a minimum of 10 completed purchases with your DIRECT debit card, refunds do not apply

If You do not hold a minimum account balance of $5,000 and/or have a minimum of ten (10) completed purchases with your Direct Debit Card, your account will default to the Classic Account.

1.9 Interest Disclosures

This Account is not interest-bearing. No interest will be paid on this Account.

1.10 Authority

You agree that we may honor and rely upon the instructions or the execution, delivery and/or negotiation of any check, substitute check, draft, withdrawal order, instruction or similar instrument (collectively, “items”) or document by any of your authorized agents regardless of the necessity or reasonableness of such action, the circumstances of any transactions affected by such action, the amount of the transaction, the source or disposition of any proceeds and regardless of whether the relevant items or documents result in payment to the authorized agent or an individual obligation of the authorized agent or anyone else. “Authorized agents” include Authorized Users and any person who has signed a signature card, who is authorized by this Agreement, any resolution or otherwise to access or use the Account. It also includes any person who has been permitted by you or another authorized agent to act on your behalf in dealing with us.

You will not deny the authenticity, validity, binding effect and authorization of any action we take in reliance upon the instructions, items or documents provided by an authorized agent unless you have previously revoked such person’s authority to access or use your Account by notifying us as specified above and we have confirmed our acceptance of your notice.

1.11 Power of Attorney and Attorneys-In-Fact

We may allow you to give another person (known as an “attorney-in-fact”) power of attorney to act on your behalf for your Account. You must obtain written approval from us before we will honor any power of attorney. Email us at the email address specified above for approval if you plan to create a power of attorney. Please be aware that it may take up to two (2) weeks for us to review your request. If approved, we will honor orders and instructions from your attorney-in-fact until (a) we receive a written revocation from you; (b) we are notified that you or your attorney-in-fact have died or become incapacitated; or (c) we terminate our acceptance of the power of attorney. We may terminate our acceptance at any time, for any reason and without notice to you, and you will not hold us liable for any Losses (as defined below) that may result from such action.

1.12 Death or Incapacitation

You agree that if we receive notification or if we have reason to believe that you or any Authorized User has died or become legally incapacitated, we may place a hold on your Account and refuse all transactions until we know and have verified the identify of your heir, devisee or successor. Until we received notice and any required proof of death or incapacitation, we may continue to accept deposits and process transactions to your Account. Your estate will be responsible for repaying us for any tax liability resulting from payment of your account balance to your estate. You will hold us harmless for any actions we take based on our reasonable belief that you have died or become incapacitated. If certain payments originating from government entities are deposited into your Account after your death, we may be required to return those payments to the originator upon notice.

1.13 Our Relationship With You

By opening an Account, we are establishing an Account relationship with you and committing to act in good faith and to the exercise of ordinary care in our dealings with you as defined by the Uniform Commercial Code as adopted by the State of Oregon. This Agreement and the Account relationship do not create a fiduciary relationship or any other special relationship between you and us.

1.14 Third-Party Service Providers

We work with one or more third-party service providers, including Unit Finance Inc. (“Unit”) and the Program Partner, in connection with your Account. You acknowledge that we, in our sole discretion, may use such third-party service providers to fulfill any of our obligations under this agreement, including by performing functions that you have otherwise authorized us to perform, such as processing transactions, handing account operations including account set-up, transaction monitoring, and customer support, and providing technological connection to the Program Partner and the Bank. Each of these third-party service providers may in turn use their own third-party service providers, at our discretion.

1.15 Confidentiality and Our Privacy Policy

Information about your Account and your transactions is collected by us, the Program Partner and our service providers. To the extent this information relates to a particular individual, this information is used and disclosed by each Party according to their published privacy policy, available at https://www.pacificwestbank.com/Privacy-Policy (for Bank), https://www.directb.net/privacy-policy (for Program Partner), and https://www.unit.co/privacy-policy (for Unit).

1.16 Cell Phone Communications

By providing us with your cellular phone or other wireless device number, you are expressly consenting to receiving communications at that number - including but not limited to prerecorded or artificial voice message calls, text messages, app notifications and calls made by an autodialer - from us and our affiliates, service providers and agents. This consent applies to all telephone numbers that you provide us now or in the future. Your telephone or mobile service provider may charge you for these calls or messages. You also agree that we may record or monitor any communications for quality control or training purposes.

1.17 Our Business Days

Our business days are Monday through Friday, excluding federal holidays and Oregon banking holidays.

2 Your Account Responsibilities

We strive to keep your Account secure and provide you with tools and services to help you manage your Account. However, there are certain things you should do to protect your Account and your funds.

2.1 Notify Us If Your Information Changes

You must notify us immediately if there is a change to your name, the names of any individual or Authorized User with access to your Account, telephone number, legal address, email address or any other information you have provided us so that we can continue to provide you with statements and important notices concerning your Account.

2.2 Keep Track of Your Transactions and Available Balance

It is important that you keep track of your transactions and the funds in your Account that are available for you to use (“Available Balance”) by reviewing your transaction history. It is also important to understand that your Available Balance may not reflect transactions you have authorized that have not yet been presented to us for payment.

You are also responsible for reviewing your Account statements as they are made available to you for errors or unauthorized activity. If you identify an error or unauthorized activity, you must notify us promptly. Please refer to the applicable sections below for information concerning errors and unauthorized activity.

2.3 Protect Your Account Information

It is important that you protect your Account information to prevent unauthorized transactions and fraud. Keep your Account number, debit card, and statements secure at all times, and be careful about who you share this information with. If the Program Partner provides you with access to Online Banking Services, make sure to also keep your computer or mobile device secure at all times and avoid accessing the Online Banking Services when others can see your screen.

If your Account number, debit card, mobile device or Online Banking Services login credentials are lost or stolen, notify us immediately to keep your losses to a minimum. Please refer below for information and applicable deadlines for notifying us of losses or theft.

3 General Rules Governing Your Account

You understand that any payment instruction or activity performed using any Online Banking Services provided to you by the Program Partner will be deemed authorized by you and valid and we are under no obligation to investigate the instruction or activity.

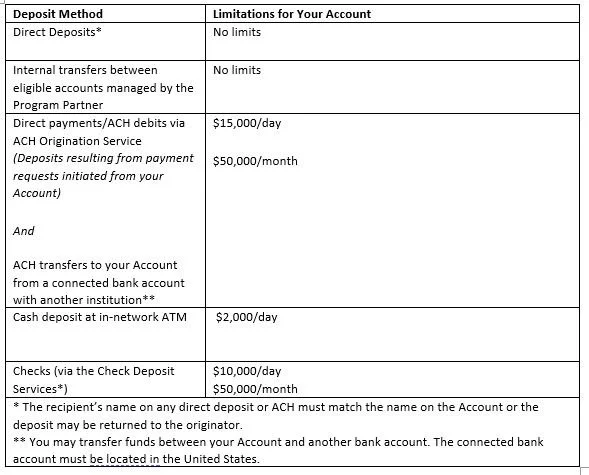

3.1 Deposits Into Your Account

You may make deposits into your Account using any of these methods described below. We do not charge you any fees for making deposits.

We do not accept cash deposits by mail, or paper check or foreign currency deposits: We are not liable for deposits of any kind that you mail to us, including if it is lost in transit, lost in the mail, or otherwise not received by us.

▪ Cash: Certain cash deposits may be available depending on the services available for your Account. We do not accept cash deposits made by mail. If you mail us a cash deposit, we will send the cash back to you.

▪ Paper Checks: If you mail a paper check to us, including personal or business checks, money orders or cashier’s checks, we may apply the check to any negative balance you have on your Account or send the check back to you.

▪ Foreign Currency: We do not accept any deposits in foreign currency. Any deposits received in foreign currency, whether in the form of cash or check, will be sent back to you.

We will send all items back to the address we have for you and we are not liable if you do not receive the items.

You may only deposit with us funds that are immediately available, which under applicable law are irreversible and are not subject to any lien, claim or encumbrance.

For more information about deposits and when funds from a deposit will be made available to you, please refer to the applicable section below.

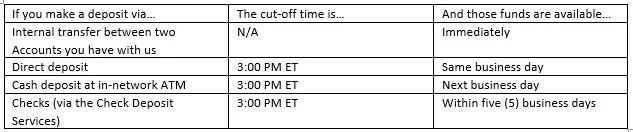

3.2 Our Funds Availability Policy

It is our policy to make deposits made to your Account each business day available for withdrawal according to the table below. The end of the business day is referred to as the “deposit cut-off time”. If you make a deposit before our cut-off time on a business day that we are open, we will consider that day to be the day of your deposit. However, if you make a deposit after our cut-off time or on a day we are not open, we will consider the deposit to be made on the next business day that we are open.

The availability of funds transferred to your Account from a connected bank account held by another financial institution follows different rules. Please refer to the section below on connected accounts for more information.

3.3 Problems that Could Occur With Deposits

If a deposit or transfer to your Account is returned or rejected by the paying financial institution for any reason, or if there is an error or mistake involving a deposit or transfer, we may deduct the amount of the deposit, transfer, or error without prior notice to you. If there are insufficient funds in your Account at the time, your Account may become overdrawn. Please refer to the section below concerning overdrafts for more information.

3.4 Transfers To or From Two Accounts You Have With Us

If you hold multiple accounts with us, we may permit you to transfer funds from one Account in your name to another account in your name held by us that is managed by the Program Partner (an “internal transfer”). The Program Partner may impose limits on such transfers as identified herein.

3.5 Withdrawals From Your Account

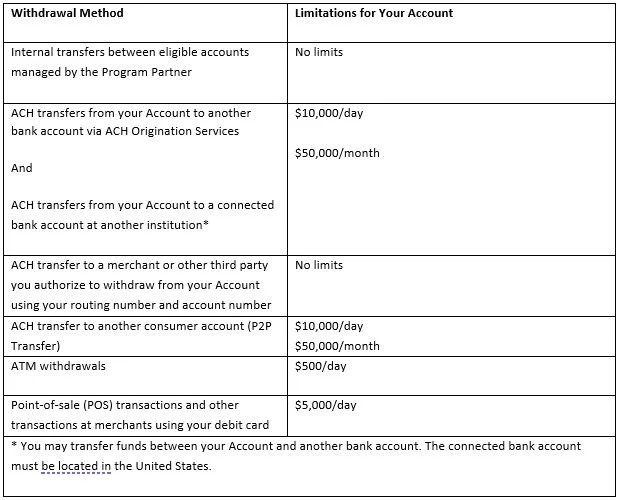

You, or, if applicable, an Authorized User, may withdraw funds using your debit card or another permitted method to access funds in your Account up to the amount of your Available Balance less applicable fees in your Account using any of the following methods and subject to the following limits:

Before permitting a withdrawal or other transaction, we may request that you provide us with additional information or documentation that we deem necessary to confirm your identity or to prevent illegal activity. We may refuse the transaction if you do not comply with our request.

3.6 Transfers To or From Connected Bank Accounts

You may be provided with the ability to link another bank account you have with another financial institution (“connected bank account”) to your Account with us to make inbound and/or outbound ACH transfers between the connected bank account and your Account through the Online Banking Services. An “inbound transfer” moves funds into your Account from a connected bank account. An “outbound transfer” moves funds from your Account to a connected bank account.

For inbound transfers, we will debit your connected bank account and credit your Account with us on the next business day after you initiate the transfer. The funds you transfer to your Account will be made available to you by the fifth (5th) business day after the business day that we debited your Account.

For outbound transfers, we will debit your Account with us and request the financial institution that holds your connected bank account to credit your connected bank account no later than the next business day after you initiate the transfer. The financial institution that holds your connected bank account determines when those funds will be made available to you in your connected bank account.

You agree that you will only attempt to connect a bank account for which you have the authority to transfer funds. You may only link a bank account that is a deposit account, such as a checking, savings or money market account.

3.7 No Illegal Activity, Internet Gambling and Right to Refuse Transactions

You must not use your Account for any illegal purposes or, regardless of whether it is legal or illegal, for online gambling of any sort, including any betting transaction, purchase of lottery tickets, casino chips, or off-track betting and wagering. We may deny any transaction or refuse to accept any deposit that we believe is related to illegal activity, online gambling or for any other reason at our discretion. However, in the event that a charge or transaction described in this section is approved and processed, you will still be liable for the charges.

3.8 Funds Transfer Services

Funds transfers to or from your Account will be governed by the rules of the funds transfer system(s) through which the transfers are made (“system rules”), including Fedwire, the National Automated Clearing House Association (NACHA), the Clearing House Interbank Payments System (CHIPS), and the Society for Worldwide Interbank Financial Telecommunication (SWIFT). We are under no obligation to honor, in whole or in part, any payment order or other instruction that could result in our contravention of applicable law, including requirements of the U.S. Department of the Treasury’s Office of Foreign Assets Control (OFAC) and the Financial Crimes Enforcement Network (FinCEN). For additional information on electronic fund transfers generally, see below. For additional information on (1) ACH transactions specifically, (2) check deposits and mobile deposit services, and (3) wire transfers, see the relevant titled sections below.

If your Account receives incoming ACH transactions (either credits or debits) or wire transfers initiated from within or outside of the United States, both you and we are subject to the Operating Rules and Guidelines of NACHA, or the rules of any wire transfer system involved, and the laws enforced by OFAC. Under such rules and laws, we may temporarily suspend processing of a transaction for greater scrutiny or verification against the OFAC list of blocked parties, which may result in delayed settlement, posting and/or availability of funds.

We reserve the right to temporarily suspend, block or reject the processing of any transaction, to freeze or block certain funds or the full balance of any Account, account owner, account beneficiary, or Authorized User (each, a “Restricted Person”), in each case to the extent we deem reasonably necessary to comply with any notice, order, regulation, rule, requirement or restriction issued or promulgated by OFAC (collectively, the “OFAC Rules”). To comply with OFAC Rules, we may temporarily suspend processing of a transaction or the availability of a balance for greater scrutiny or verification against the OFAC list of blocked parties, which may result in delayed settlement, posting and/or availability of funds. If we determine there is a violation or potential violation of the OFAC Rules, or if we cannot satisfactorily resolve a suspected or potential violation, we may reject such transaction or freeze or block the subject funds or full balance of any Account or Restricted Person. If we block the subject funds and you believe you have adequate grounds to seek the return of any blocked funds, it is your sole responsibility to pursue the matter with the appropriate governmental authorities. Please see the OFAC website for procedures and form required to seek a release of blocked funds.

You also will observe all anti-money laundering and exchange control laws and regulations, including economic and trade sanctions promulgated by OFAC, in relation to any funds transfer, and you will use all reasonable efforts to assist us to do likewise. You warrant that the information given to us by you is accurate. We may disclose any information given to us that we in our sole discretion think necessary or desirable to disclose; except we will only disclose confidential information if required by law, a court, or legal, regulatory, or governmental authority, or as permitted by law to combat, prevent, or investigate issues arising under anti-money laundering laws, economic sanctions, or criminal law.

Sometimes legal, regulatory, or governmental authorities require additional information, either in respect of individuals, entities, or particular transactions. You warrant that you will promptly supply all such information, which any such authority may require, and/or which we may be required to supply, in relation to the individual, entity, or particular transaction.

If you, or your Authorized User, breach any such laws or regulations, you irrevocably agree that we may retain any monies or funds transmitted to us pursuant to this Agreement and/or not fulfill any funds transfer request if we are required to take or refrain from such action by any legal, regulatory, or governmental authority or if we reasonably believe that such action may violate any laws or regulations described herein, and such monies will not bear interest against us. You further agree that we may pay such monies to the appropriate legal, regulatory, or governmental authority, when required by law or regulation.

3.9 How We Post Transactions To Your Account and Determine Your Available Balance

3.9.1 Posting Overview

To understand how we post transactions to your Account, it is important to first understand the difference between your Available Balance and your ledger balance. Your Available Balance is the amount of money you have in your Account at any given time that is available for you to use. Your ledger balance is the balance in your Account at the beginning of the day after we have posted all transactions to your Account from the day before. We use your Available Balance to authorize your transactions throughout the day and determine whether you have sufficient funds to pay your transactions. Here are some additional terms that are helpful to understand:

▪ Credit and debit – A credit increases your balance and a debit decreases your balance.

▪ Post or posted – Transactions that are paid from or deposited to your Account. Posted transactions will either increase or decrease both your Available Balance and your ledger balance.

▪ Pending – Transactions that we receive notice of and are scheduled to post to your Account. Pending transactions affect your Available Balance, but not your ledger balance.

▪ Card authorization and settlement – When you use a debit card to make a purchase, the transaction occurs in two steps: card authorization and settlement. Card authorizations reduce your Available Balance, but not your ledger balance. Settlement reduces both your Available Balance and your ledger balance. Card authorizations are removed when settlement occurs or after a certain number of days have passed, whichever is sooner. See below for more information about card authorizations and settlement.

3.9.2 Posting Order

We receive the transactions throughout the day and post them to your Account as they are received and in the order that they are received. Note that for debit card transactions, we consider the transaction received when the merchant requests settlement, which may occur several days after you authorize the transaction. See below for additional information concerning how debit card transactions are processed.

If we change the order in which we post transactions to your Account, we will provide advance notice. It is important for you to keep track of the deposits you make and the transactions you authorize to make sure there are sufficient funds in your Account to cover all transactions and any applicable fees.

3.9.3 Determining Your Ledger Balance and Available Balance

Your Account’s ledger balance is the current balance of cleared and settled funds in your Account at the beginning of each business day. Your Account’s Available Balance is the ledger balance reduced by items we receive throughout the day. To determine your Available Balance, we start with your ledger balance at the beginning of the business day, add any pending credits or deposits that we make available to you, and subtract any card authorizations and pending debits. All transactions are debited or credited from your Available Balance in the order received.

Your balance is accessible through the Online Banking Services or as otherwise indicated herein. Keep in mind that your Available Balance may not reflect every transaction you have initiated or previously authorized. For example, your Available Balance will not include transactions you have authorized that we have not received.

3.9.4 Debit Card Authorizations

If you are issued a debit card with your Account, you will be able to use your card to pay for goods or services or to conduct other transactions with a merchant. When you engage in a transaction with a merchant using your debit card, the merchant will request preauthorization (“card authorization”) for the transaction. If there are sufficient available funds in your Account, we will approve the request and reduce your Available Balance for as long as the card authorization remains on your Account.

Your Available Balance will generally be reduced by the amount of the card authorization. If you use your card at a restaurant, your Available Balance may be reduced by the amount of the card authorization plus up to an additional twenty percent (20%) of that amount, to account for potential tipping.

The card authorization will remain on your Account until the merchant sends us the final amount of the transaction and requests payment (“settlement”). In most cases, If the merchant does not request settlement, or the merchant is delayed in requesting settlement, the card authorization will automatically be removed after three (3) days. However, for certain merchants such as hotels and rental car companies, it may take up to thirty (30) days for the card authorization to be removed.

It is important to understand that the merchant controls the timing of card authorizations or settlement. A merchant may request settlement after the card authorization has been removed from your Account. This means that if you use the funds in your Account after the card authorization has been removed and the merchant later requests settlement, your Account may become overdrawn. A merchant may also request settlement for an amount that is different than the card authorization. Therefore, it is important that you keep track of your transactions and your balance. Once we have approved a card authorization, we cannot stop the transaction and you will be responsible for repaying any negative balance that may occur.

3.10 Statements

Statements will periodically be provided to you by through the Online Banking Services as long as your Account is not inactive. You will receive a statement monthly as long as you have transactions on your Account during the statement period. If there were no transactions on your Account, we may provide you with statements on at least a quarterly basis. You will not receive paper statements.

3.11 Errors On Your Account and Limitations of Liability

You will carefully review your statements for your Account and will promptly report to us any errors or unauthorized activity by email at the address indicated above within sixty (60) days after we make the statement available to you. Unless otherwise specified in this Agreement or required by law, if you do not provide us with timely notice of an error or unauthorized activity, we will deem our records concerning your Account and all cards to be correct and we will not be liable to you for any Loss you suffer relating to the error or unauthorized activity. You further agree that we may debit or credit your Account at any time and without notice to you to correct an error or address unauthorized activity.

Please refer to the relevant section below for additional information concerning errors and unauthorized transactions involving electronic fund transfers and related limitations of liability.

3.12 Overdrafts, Nonsufficient Funds and Negative Balances

An overdraft occurs when you do not have enough money in your Account to cover a transaction, but we pay it anyway. We do not permit you to overdraw your Account.

However, there may be instances where your Account can still go into the negative, such as if a deposit you make is returned.

You must make a deposit immediately to cover any negative balance. If your Account has a negative balance for sixty (60) calendar days or more, we may close your Account, and we reserve the right to close the Account an earlier date, as permitted by law.

3.13 Closing Your Account and Account Suspensions

You can close your Account at any time and for any reason by email at the contact provided above. We reserve the right to refuse your request if you have a negative balance on your Account. We recommend that you transfer or withdraw any funds you may have in the Account prior to submitting a request to close the Account to avoid delays in receiving your funds.

We may also suspend or close your Account, or suspend, or disable any service or feature of your Account, at our discretion with or without notice. This includes if we believe you are using your Account for fraudulent or illegal purposes or in violation of law or regulation, this Agreement, any other agreement you may have with us, if multiple transactions are returned on your Account, or if you otherwise present undue risk to us.

Accounts with a zero balance will continue to be charged applicable fees until you request to close your Account. We may close an Account with a zero balance on the fee period ending date or at month end without prior notification to you. Once an Account is closed (either by you or us), no fees will be assessed on the Account.

We may also close your Account if you have not made any deposits or withdrawals from your Account in over twelve (12) months. In addition, canceling your enrollment in the Online Banking Services with the Program Partner will result in our closure of the Account and our return of your funds.

If your Account is closed with a balance greater than $1.00, we will return any funds you may have in the Account to you by ACH transfer to another bank account or by paper check. We reserve the right not to return the funds to you if the balance in your Account is $1.00 or less.

We are not responsible to you for any damages you may suffer as a result of the closure or suspension of your Account. The closure of your Account or termination of this Agreement does not impact any right or obligation that arose prior to closure or termination, or any right or obligation that, by its nature, should survive termination (including all indemnifications obligation by you, our limitations of liability, and all terms governing arbitration).

3.14 Dormancy, Inactivity and Unclaimed Property

State law and our policy govern when your Account is considered dormant. Your Account is usually considered dormant if you have not accessed your Account, communicated to us about your Account or otherwise shown an interest in your Account within the period of time specified under applicable law. Each state has varying laws as to when an account becomes dormant, and we may be required to send the balance in your Account if it becomes dormant to the state of your last known address. We will make reasonable efforts to contact you if required by applicable law before transferring the remaining balance of your Account to the applicable state. After we surrender the funds to the state, you must apply to the appropriate state agency to reclaim your funds. You can avoid the surrender of your funds by simply conducting transactions, contacting us about your Account or replying to any abandoned property notices we may provide to you.

We may also place your Account in an inactive status if you have not had any transaction for at least six (6) months. If your Account becomes inactive, you may not receive statements or be able to conduct certain transactions. Inactive Accounts must be reactivated. Contact us to reactivate your Account.

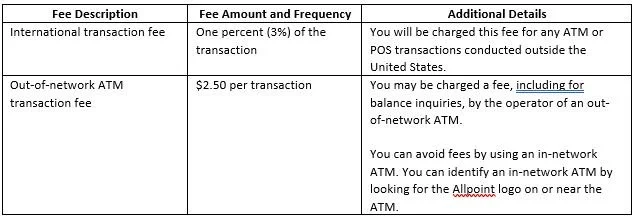

3.15 Account Fees and Fee Schedule

You will pay all fees and charges applicable to your Account. All fee amounts will be withdrawn from your Account and will be assessed regardless of whether you have sufficient funds in your Account, except where prohibited by law. Fees are subject to change at any time. We will provide you advance notice of any changes where required by law.

4 Electronic Fund Transfers

Your Account allows you to withdraw funds up to the Available Balance or make deposits through electronic fund transfers (“EFTs”). EFTs are transactions that are processed by electronic means and include, among others, ACH transfers, debit card transactions and direct deposits. This Section provides you with information and important disclosures and terms about the EFTs that are permitted on your Account. You may also receive additional services through Online Banking Services provided by the Program Partner, that allow you to initiate EFTs to and from your Account that are not described in this Agreement. In the event the Program Partner provides such additional services, you will be provided separate agreements and disclosures applicable to those services by the Program Partner.

4.1 Types of EFTs Supported by Your Account

Depending on the features made available for your Account by the Program Partner, your Account may support the following types of EFTs:

▪ Direct deposits from your sources of income

▪ Transfers to or from your Account to or from a connected bank account

▪ Transfers from your Account to another person’s bank account using the P2P Transfer Service

▪ Transfers to or from your Account to a merchant or other third party by providing the third party with your Account routing number and account number.

▪ Purchases or other transactions using your debit card.

▪ ATM deposits or withdrawals using your debit card.

4.2 Limitations on EFTs

There are limitations on the frequency and amount of transactions you can make to or from your Account. These limits are different for each type of transaction. For limits that apply to transactions that credit or deposit funds into your Account, please refer above for information concerning deposits. For limits that apply to transactions that debit or withdraw from your Account, please refer above to the section concerning withdrawals. These security-related limits may change from time to time.

If you have been issued a debit card for your Account, there may also be transaction limitations that apply to your use of the card. Please refer to the applicable cardholder agreement provided to you with your card for information on any limitations and other terms.

4.3 Your Right to Receive Information and Documentation of Your Transactions

You will receive information and documentation concerning any EFTs that debit or credit your Account in the following ways:

▪ Statements: We will provide you information about each transaction that debits or credits your Account on your statements. Please refer above for information about statements.

▪ Direct Deposits: If you receive a direct deposit into your Account at least once every sixty (60) days from your employer or other person or company, you can check if the deposit has been made through the Online Banking Systems or by contacting us as detailed above.

▪ Receipts: You can get a receipt at the time you make a withdrawal at an ATM or a purchase at a point-of-sale terminal using your debit card. However, for certain small dollars transactions you may not receive a receipt.

4.4 Preauthorized Transfers, Stop Payments and Notices of Varying Amounts

If you authorize us or another company or person to withdraw from your Account on a regular basis (such as when you sign up for “autopay” to pay a recurring bill or invoice), it is called a “Preauthorized Transfer.” You may request that we place a stop payment on Preauthorized Transfers, as well as get notification when the amount of a particular withdrawal will be different from the amount of the last withdrawal. We may charge a fee to stop payment on Preauthorized Transfers (as outlined in the fees section above).

4.4.1 How to Request a Stop Payment

If you authorize a third party to take payments from your Account on a regular basis through a Preauthorized Transfer, you can place a stop payment on those payments by contacting us by email at the address listed above at least three (3) business days before the next payment is scheduled to be made. To be effective, a stop payment request must be received within this time specified, and with all of the information required below, so as to give a reasonable opportunity to act on it.

You must provide: (a) your name, (b) your Account number, (c) the company or person taking the payments, and (d) the date and amount of the Preauthorized Transfer you wish to stop. If you want all future payments from that company or person stopped, be sure to tell us that as well. If you do not provide us with the correct information, such as the correct payee or the correct amount of the payment you wish to stop, we may not be able to stop the payment.

4.4.2 Our Liability if We Fail To Stop a Preauthorized Transfer

If you order us to stop one of these payments three (3) business days or more before the payment is scheduled and provide us with all information requested, and we do not do so, we will be liable for your losses or damages proximately caused by the failure. However, we will not be liable if the company or person initiating the payments changes the dollar amount of the payment or makes other changes that cause us not to recognize it as the payment you requested be stopped.

It is your responsibility to ensure that all of the information supplied in your notice is correct and to promptly inform us of any inaccuracies. We are not liable for failing to stop payment if you have not given us sufficient information or if your stop payment request comes too late for us to act on it. If we stop payment, you will indemnify, defend and hold us and our officers, directors, shareholders, employees, successors, predecessors, representatives, principals, agents, assigns, parents, subsidiaries and/or insurers (collectively, "Indemnified Parties") harmless from any and all losses, liabilities, costs, and expenses (including reasonable fees and expenses for attorneys, experts and consultants, reasonable out-of-pocket costs, interest and penalties), settlements, fines, fees, penalties, equitable relief, judgments, and damages ("Losses") imposed on or sustained, incurred or suffered by any of the Indemnified Parties, whether actual or threatened or proven or not, in respect of any and all actions, audits, arbitrations, assertions, suits, mediations, litigations, proceedings, examinations, hearings, inquiries, investigations, charges, complaints, claims (including counter or cross-claims), or demands by whosoever asserted ("Claims"), without regard to the merit or lack thereof, arising from or related in any way to our refusal to pay the transaction on which you stopped payment. The foregoing indemnity will not apply if and to the extent expressly prohibited or restricted by the laws or regulations governing you or your Account.

4.4.3 Notices of Varying Amounts

If these regular payments vary in amount, the person or company you are paying should tell you ten (10) days before each payment when it will be made and how much it will be. You may be given the option to only get this notice when the payment will differ by more than a certain amount from the previous payment, or when the amount will fall outside certain limits that you set.

4.5 Our Liability for a Failure To Complete A Transaction

If we fail to complete a transaction on time or in the correct amount when properly instructed by you in accordance with this Agreement, we will be liable for damages proximately caused by the failure or error. However, there are some exceptions. We are not liable, for instance:

▪ If the Available Balance in your Account is not sufficient to complete the transaction through no fault of ours;

▪ If the ATM you use does not have enough cash;

▪ If the failure is due to an equipment or system breakdown, such as a problem with the Online Banking Services provided by the Program Partner, that you knew about before you began a transaction;

▪ The failure was caused by an Act of God, fire or other catastrophe, or any other cause beyond our control despite reasonable precautions we have taken;

▪ If your funds are not available due to a hold or if your funds are subject to legal process;

▪ If we do not complete a transaction because we or Unit has reason to believe the transaction is unauthorized or illegal;

▪ If your Account is closed or inactive;

▪ There may be additional exceptions stated in our or our service provider’s agreements with you or permitted by law.

4.6 Your Liability for Unauthorized EFTs

Contact us immediately if you believe that an unauthorized EFT has occurred or may occur concerning your Account, or if your debit card or Online Banking Services login credentials have been lost, stolen or compromised. Calling us at 503-344-1230 is the best way of keeping your losses to a minimum.

You could lose all the money in your Account (and any bank accounts with other institutions you have connected to your Account) if you take no action to notify us of the unauthorized EFT or the loss or theft of your debit card, or Online Banking Services login credentials.

For unauthorized EFTs, your liability will be as follows if you notify us of the loss:

▪ If you tell us within two (2) business days after learning of the loss, theft or compromise of your Online Banking Services login credentials, you can lose no more than $50.

▪ If you do NOT tell us within two (2) business days and we can prove that we could have prevented the loss had you contacted us, you could lose as much as $500.00.

▪ If your statement shows EFTs that you did not make and you do NOT contact us within sixty (60) days after the statement was made available to you, you may not get back any money lost after the sixty (60) days if we can prove that your contacting us would have prevent those losses.

We can extend these time periods if extenuating circumstances (such as a long trip or hospital stay) kept you from notifying us.

If you believe an unauthorized transaction has occurred concerning your Account, or if your debit card or Online Banking Services login credential have been lost or stolen, contact us at indicated above.

4.7 In Case of Errors or Questions About Your EFTs

Contact us as soon as you can if you think your statement or receipt is wrong or if you need more information about a transfer listed on a statement or receipt. For card related transactions, contact us at 1-833-333-0417; for all other transactions call us at the phone number or email address listed above. We must hear from you no later than sixty (60) days after we send the FIRST statement on which the problem or error appears. You must provide us with the following information:

▪ Your name and Account number;

▪ A description of the error or the EFT you are unsure about and why you believe it is an error or you need more information; and

▪ The dollar amount of the suspected error.

If you tell us orally, we may require that you send us your complaint or question in writing by email within ten (10) business days.

We will determine whether an error occurred within ten (10) business days after we hear from you and will provide you the results and correct any error promptly. If we need more time, we may take up to forty-five (45) days—or ninety (90) days for Accounts open less than thirty (30) days or foreign-initiated transactions — to investigate your complaint or question. If we decide to do this, we will credit your Account within ten (10) business days for the amount you think is in error, so that you will have the use of the money during the time it takes us to complete our investigation. If we ask you to put your complaint or question in writing and we do not receive it within ten (10) business days, we may not credit your account. For Accounts open less than thirty (30) days, we may take up to twenty (20) business days to credit your Account for the amount you think is in error.

We will provide you the results within three (3) business days after completing our investigation. If we decide that there was no error, we will send you a written explanation by email. You may ask for copies of the documents that we used in our investigation.

5 P2P Transfer Service

5.1 Description of P2P Transfer Service

If enabled for your Account, the P2P Transfer Service will allow you to send funds from your Account to another person’s bank account through the Online Banking Services. You will need to know the routing number and account number for the other person’s bank account to initiate a transfer. The P2P Transfer Service only permits you to send funds. You may not use it to receive or request funds. All transfers made through the P2P Transfer Service will be executed as ACH transfers in accordance with the rules promulgated by the National Automated Clearing House Association (“NACHA”). Your use of and access to the P2P Transfer Service is separate and apart from your ability to facilitate transfers via ACH to a connected bank account (see above).

5.2 Transaction Deadlines

Our cut-off time for P2P transfer requests is 3:00 PM ET on business days. Requests received before our cut-off time will be processed that day. Requests received after our cut-off or on a non-business day will be processed the next business day. For purposes of P2P transfers, a “business day” is a day in which the Federal Reserve Bank is opened to the public for carrying on substantially all of its business, other than a Saturday, Sunday, or legal holiday.

5.3 P2P Transfer Limits

There are limitations on the frequency and amount of P2P transfers you can make from your Account using the P2P Transfer Service. These limits are described in the relevant section of this Agreement. These security-related limits may change from time to time.

5.4 Provisional Credit

You acknowledge that any credit given to the account of the person you are transferring funds to through the P2P Transfer Service will be provisional until the financial institution crediting that account receives final settlement of your funds. This means that the person you transfer funds to will not be considered to be paid by you until final settlement occurs, and any provisional credit given to that person by their financial institution before settlement may be taken back if settlement does not occur.

5.5 Cancellation or Modification of Transfer Requests

Once you authorize a P2P transfer through the P2P Transfer Service, you will not be able to cancel or modify the transfer.

5.6 Prohibited Transactions and Rejection of P2P Transfers

You agree that you will not use the P2P Transfer Service to initiate transfers related in any way to online gambling, or that would violate any law or regulation. You further agree that you will only use the P2P Transfer Service to initiate transfers to consumer bank accounts. You may not use the P2P Transfer Service to transfer funds for any business purpose or to a business-purpose bank account.

We may block a transfer and/or take any other action we deem reasonable if we suspect that a transaction is unlawful, suspicious, related to online gambling, for a business purpose, or poses undue risk to us or any of our service providers. We will not be liable for any damages that arise if we block a transfer or take any other action pursuant to this paragraph.

5.7 Returned P2P Transfers

We will notify you by email or via the Online Banking Services of a transfer you have requested is returned to us no later than one (1) business day after the business day we receive notice of the return. We will not reattempt any transfer that is returned.

We reserve the right to suspend or terminate your access to the P2P Transfer Service if an excessive number of P2P transfers are returned.

5.8 Fees

You will pay for the P2P Transfer Service provided under the Agreement in accordance with the current schedule of fees above. Fees may change from time to time upon written notice.

5.9 P2P Transfer Service Liability, Limitations on Liability & Indemnity

WE SHALL BE RESPONSIBLE ONLY FOR PERFORMING THE P2P TRANSFER SERVICE EXPRESSLY PROVIDED FOR IN THIS AGREEMENT AND SHALL BE LIABLE ONLY FOR OUR GROSS NEGLIGENCE IN PERFORMING THIS SERVICE. WE SHALL NOT BE RESPONSIBLE FOR YOUR ACTS OR OMISSIONS (INCLUDING THE AMOUNT, ACCURACY, TIMELINESS OF TRANSMITTAL OR AUTHORIZATION OF ANY P2P TRANSFER REQUEST FROM YOU) OR THOSE OF ANY OTHER PERSON. WE ARE AUTHORIZED BY YOU TO PROCESS P2P TRANSFERS IN ACCORDANCE WITH THE INFORMATION THAT WE RECEIVE FROM YOU. YOU SHALL BE SOLELY RESPONSIBLE FOR THE INFORMATION YOU PROVIDE TO US, AND WE SHALL HAVE NO RESPONSIBILITY FOR ERRONEOUS DATA PROVIDED BY YOU. YOU WILL INDEMNIFY AND HOLD US HARMLESS FROM AND AGAINST ANY LOSS, CHARGE, LIABILITY, COST, FEE OR EXPENSE (INCLUDING ATTORNEYS’ FEES AND EXPENSES) WE SUFFER OR INCUR RESULTING FROM ANY THIRD-PARTY LAWSUIT, CLAIM, ARBITRATION OR OTHER ACTION, ACTUAL OR THREATENED, ARISING UNDER OR IN CONNECTION WITH THIS AGREEMENT.

IN NO EVENT SHALL WE BE LIABLE FOR ANY CONSEQUENTIAL, SPECIAL, PUNITIVE, OR INDIRECT LOSS OR DAMAGE THAT YOU MAY INCUR OR SUFFER IN CONNECTION WITH THIS AGREEMENT, INCLUDING LOSSES OR DAMAGES FROM SUBSEQUENT WRONGFUL DISHONOR RESULTING FROM OUR ACTS OR OMISSIONS PURSUANT TO THIS AGREEMENT.

WITHOUT LIMITING THE GENERALITY OF THE FOREGOING PROVISIONS, WE SHALL BE EXCUSED FROM FAILING TO ACT OR DELAY IN ACTING IF SUCH FAILURE OR DELAY IS CAUSED BY LEGAL CONSTRAINT, INTERRUPTION OF TRANSMISSION OR COMMUNICATION FACILITIES, EQUIPMENT FAILURE, WAR, NATURAL DISASTER, EMERGENCY CONDITIONS, OR OTHER CIRCUMSTANCES BEYOND OUR CONTROL. NOTWITHSTANDING THE ABOVE, WE WILL REIMBURSE YOU FOR EXPENSES INCURRED IN THE EVENT OF OUR FAILURE OR DELAY IN TRANSFERRING FUNDS SOLELY CAUSED US.

IN ADDITION, WE SHALL BE EXCUSED FROM FAILING TO TRANSMIT OR DELAY IN TRANSMITTING A P2P TRANSFER IF SUCH TRANSMITTAL WOULD RESULT IN OUR HAVING EXCEEDED ANY LIMITATION UPON OUR INTRA-DAY NET FUNDS POSITION ESTABLISHED PURSUANT TO PRESENT OR FUTURE FEDERAL RESERVE GUIDELINES OR IN OUR REASONABLE JUDGMENT OTHERWISE VIOLATE ANY PROVISION OF ANY PRESENT OR FUTURE RISK CONTROL PROGRAM OF THE FEDERAL RESERVE, OR ANY RULE OR REGULATION OF ANY OTHER U.S. GOVERNMENTAL REGULATORY AUTHORITY. SUBJECT TO THE FOREGOING LIMITATIONS, OUR LIABILITY FOR LOSS OF INTEREST RESULTING FROM ITS ERROR OR DELAY SHALL BE CALCULATED BY USING A RATE EQUAL TO THE AVERAGE FEDERAL FUNDS RATE SET BY THE FEDERAL RESERVE BANK FOR THE PERIOD INVOLVED. AT OUR OPTION, PAYMENT OF SUCH INTEREST MAY BE MADE BY CREDITING THE ACCOUNT RESULTING FROM OR ARISING OUT OF ANY CLAIM OF ANY PERSON WE ARE RESPONSIBLE FOR, ANY ACT OR OMISSION OF YOU OR ANY OTHER PERSON.

5.10 Inconsistency of Name and Account Number

You acknowledge that, if the name you provide to us of the person to whom you wish to transfer funds does not match the name on the bank account you enter through the P2P Transfer Service, the transfer may still be made based only on the account number. You are solely responsible for providing correct information for all P2P Transfer Service requests through the Online Banking Services.

5.11 Termination

We reserve the right to terminate, suspend, or modify the P2P Transfer Service, or your access to the P2P Transfer Service, at any time and for any reason.

You will remain responsible for all transactions that occur prior to termination and for any fees and charges incurred prior to the date of cancellation. Any unprocessed transactions including future dated transactions, will be cancelled as a result of termination or suspension of your P2P Transfer Service.

6 Check Deposits, Mobile Deposit Services

As defined in the Check Clearing for the 21st Century Act (“Check 21”), a “check” is a draft, payable on demand and drawn on or payable through or at an office of a bank, whether or not negotiable, that is handled for forward collection or return, including substitute checks (see below) and travelers checks.

You can only deposit checks into the Account using the mobile check deposit services (the “Check Deposit Services,” as further described herein) and only as made available in connection with your Account and in accordance with the terms of this Agreement.

6.1 Substitute Checks and Your Rights

Federal rules for Check 21 allow banks to replace original checks with “substitute checks,” as defined in Check 21. Below are the details and your rights related to substitute checks.

6.1.1 Substitute Checks

To make check processing faster, federal law permits banks to replace original checks with “substitute checks.” These checks are similar in size to original checks with a slightly reduced image of the front and back of the original check. The front of a substitute check states: “This is a legal copy of your check. You can use it the same way you would use the original check.” You may use a substitute check as proof of payment just like the original check.

Some or all of the checks that you receive back from us may be substitute checks. This notice describes rights you have when you receive substitute checks from us. The rights in this notice do not apply to original checks or to electronic debits to your account. However, you have rights under other law with respect to those transactions.

6.1.2 Your Rights Regarding Substitute Checks

In certain cases, federal law provides a special procedure that allows you to request a refund for losses you suffer if a substitute check is posted to your account (for example, if you think that we withdrew the wrong amount from your account or that we withdrew money from your account more than once for the same check). The losses you may attempt to recover under this procedure may include the amount that was withdrawn from your account and fees that were charged as a result of the withdrawal (for example, bounced check fees).

The amount of your refund under this procedure is limited to the amount of your loss or the amount of the substitute check, whichever is less. You also are entitled to interest on the amount of your refund if your account is an interest-bearing account. If your loss exceeds the amount of the substitute check, you may be able to recover additional amounts under other law. If you use this procedure, you may receive up to $2,500 of your refund (plus interest if your account earns interest) within ten (10) business days after we received your claim and the remainder of your refund (plus interest if your account earns interest) not later than forty-five (45) days after we received your claim.

We may reverse the refund (including any interest on the refund) if we later are able to demonstrate that the substitute check was correctly posted to your account.

6.1.3 Claims for a Refund

If you believe that you have suffered a loss relating to a substitute check that you received and that was posted to your account, please contact us at one of the methods listed above. You must contact us within forty (40) days of the date that we delivered the substitute check in question or the account statement showing that the substitute check was posted to your account, whichever is later. We will extend this time period if you were not able to make a timely claim because of extraordinary circumstances.

Your claim must include:

● A description of why you have suffered a loss (for example, you think the amount withdrawn was incorrect);

● An estimate of the amount of your loss;

● An explanation of why the substitute check you received is insufficient to confirm that you suffered a loss; and

● A copy of the substitute check and/or the following information to help us identify the substitute check: the account number, the check number, the name of the person to whom you wrote the check, the date paid, and the amount of the check.

Substitute checks should only be generated by banks during the check collection process. If you deposit a substitute check that was not generated or previously handled by us, you agree to provide the substitute check warranties as required by Check 21, and represent that the substitute check:

● is properly generated and accurately, clearly and completely represents all the information on the front and back of the original check as of the time the original check was truncated

● bears a magnetic ink character recognition (MICR) encoded line that is suitable for automated processing in the same manner as the original check

● has not previously been paid by the drawee bank, and

● is not fraudulent

A breach of any Check 21 warranty may result in the substitute check being charged back against your account.

6.2 Mobile Check Deposit Services

The Check Deposit Services allow you to make deposits to your Account from a compatible mobile device by scanning or photographing checks and delivering the images and associated deposit information to us or our designated processor. By using the Check Deposit Services, you agree to comply with all applicable laws and regulations and NACHA rules that apply to remote deposit check capture processing and ACH transaction processing.

6.2.1 Eligibility to Use the Check Deposit Services

Accountholders adhering to all requirements described herein may be eligible to use the Check Deposit Services. Not all Accounts are eligible for the Check Deposit Services. We may terminate your use of the Check Deposit Services at any time at our sole discretion. You may also stop using the Check Deposit Services at any time. However, any images or information transmitted through your use of the Check Deposit Services will continue to be subject to this Agreement after termination. We may change our eligibility criteria at any time with or without notice to you.

To use the Check Deposit Services, you must have an internet-enabled iOS or Android device with a camera, be enrolled in the Online Banking Service, and have downloaded our latest version of the Program Partner’s mobile application containing the Check Deposit Services functionality.

6.2.2 Eligible Items

You agree that the only images you will scan or capture and deposit (“transmit”) to your Account through use of the Check Deposit Services will be Eligible Items. “Eligible Items” include paper items that are defined as “checks” or “certified checks” under Federal Reserve Regulation CC and other paper items not otherwise prohibited by this Agreement. You agree that images deemed to be Ineligible Items (see below) may not be transmitted to your Account and will be rejected by us. You further agree that the image of the Eligible Item transmitted to us will be deemed an “item” within the meaning adopted in the Uniform Commercial Code of the State of Oregon.

6.2.3 Ineligible Items

You agree you will not use the Check Deposit Services to scan or deposit images of items that:

● are not payable in United States currency;

● are not drawn on a financial institution located in the United States;

● are payable to someone other than you;

● are money orders, savings bonds, or traveler’s checks;

● are checks authorized over the telephone and created remotely;

● are images of a check that never existed in paper form;

● must be authorized or activated by us prior to being deposited;

● have already been deposited by or returned to you;

● are not legible or do not conform to our standards, as determined in our sole discretion;

● are fraudulent, not authorized, suspicious or not likely to be honored;

● are not dated, are post-dated, or are more than six (6) months old when transmitted;

● do not comply with the requirements established from time to time by any applicable statute, regulation, regulatory agency, clearing house or association;

● we deem to be Ineligible Items herein or at any other time, with or without prior notice to you;

● do not comply with the requirements of the Agreement; or

● do not meet the Technical Requirements described above.

These items, collectively, are “Ineligible Items” under this Agreement, and they are not eligible for deposit into your Account via the Check Deposit Services.

6.2.4 Image Capture, Transmission, Processing and Payment

All images you transmit to us using the Check Deposit Services must comply with the technical requirements we may specify from time to time (the “Technical Requirements”). You are responsible for all expenses you incur to meet the Technical Requirements. We reserve the right to change the Technical Requirements at any time without prior notice.

You are responsible for reviewing and validating the accuracy and completeness of any information you transmit to us, including the amount indicated on the item and the legibility of the image transmitted. You will only submit check images that meet our quality standards. You will not transmit an image or images of the same check to us more than once and will not deposit or negotiate, or seek to deposit or negotiate, such check or item with us or any other party. You will be solely responsible for the selection, use and operation of the mobile device you use to transmit images.

We can attempt to process, collect, present for payment, return or re-present images you attempt to transmit in any way we choose that is allowed by law.

We can also reject any transmission for any reason at our option and without liability. An image will be deemed received when you receive a confirmation from us that we have received the image. Receipt of such confirmation does not mean that the transmission was an Eligible Item or accepted.

If an image does not meet our requirements, we can also at our option:

● process the image as received for payment;

● correct the image or its accompanying data and process the corrected image for payment;

● process the deposit for payment in another format as allowed; or

● debit (chargeback) your Account for the amount indicated in the image.

Successfully transmitting an image to us does not mean that your transmission and deposit are complete. All of your images are subject to our further verification prior to being accepted for deposit and payment. Do not destroy the item transmitted as an image until you see the full deposit amount posted when you view your transaction history via the Online Banking Services.

6.2.5 Limits for the Check Deposit Services

There may be limitations on the frequency and amount of transactions you can make using the Check Deposit Services. Please refer to the section above concerning deposit limitations for information on transaction limitations that will apply to your use of the Check Deposit Services.

6.2.6 Required Endorsements on Items You Deposit and Managing the Original Item

When you transmit an image to us, you will still have possession of the original item. To prevent an additional submission of the item for payment, you are required take the following steps:

● Before you transmit an image to us, you must endorse the original item being captured for transmission by signing the back of the original item and writing the words “For mobile deposit only at Pacific West Bank” either above or below your signature.

● After you transmit the image to us, you should write the date and the words “Deposited by Check Deposit Services” on the front of the item and keep the original item in a safe place.

You should not deposit or attempt to cash the item after transmitting the image to us.

6.2.7 Availability of Your Deposits Using the Check Deposit Services

You acknowledge that items transmitted using the Check Deposit Services are not subject to the funds availability rules contained in Regulation CC. Funds deposited using the Check Deposit Services will ordinarily be made available to you for withdrawal within five (5) business days after the day you make your deposit. See below for information concerning how we determine the day your deposit is made. We may make such funds available sooner or later based on the length and extent of your relationship with us, transaction and experience information, and other security and risk-related factors as we, in our sole discretion, deem relevant

6.2.8 Cutoff Times for Deposits Using the Check Deposit Services

If you successfully transmit an image to us before the cutoff time for the Account on a business day that we are open, we will consider that day to be the day of your deposit. After that time or on a day we are not open, we will consider the deposit to be made on the next business day that we are open.

6.2.9 Errors

You agree to notify us of any suspected errors regarding items transmitted through the Check Deposit Services right away, and in no event later than sixty (60) days after the first Account statement on which the error appears is made available to you. Unless you notify us of an error within sixty (60) days after the applicable Account statement is made available to you, all deposits made through the Check Deposit Services that appear on that statement will be deemed correct and we will have no obligation to investigate any claim of error you make.

6.2.10 Chargeback

We can charge back your Account or any other deposit account you have with us for the amount of any item, its image or any other representation of an item that is:

● returned to us; or

● is rejected by us for any reason, including when we believe it has been previously submitted or deposited with us or with anyone else.

This is true even if you have made withdrawals against any amount we have credited to your Account for the deposited item that was returned or rejected.

We can also charge fees connected to the chargeback as described in your Account Agreement and any other agreements you have with us.

6.2.11 Fees

There may be fees associated with your use of the Check Deposit Services. Please refer to the section on fees above for all fee information.

6.2.12 Security

You are responsible for protecting your mobile device against unauthorized use as well as any Losses from unauthorized access. You will protect your mobile device, set up strong passwords and take other reasonable security precautions to protect your mobile device from unauthorized use. Always keep your passwords secret and remember that neither we nor any of our employees or agents will ever ask for your password. If you receive a communication from anyone requesting that you provide your password, do not respond. We are not responsible or obligated for any of these security precautions. If another person uses the Check Deposit Services with your mobile device, you will be responsible for their actions on the Account as well as anyone else they allow to use your mobile device. This will be true even if you did not want, or agree to, their use.

If your mobile device is lost or stolen, or if you believe there has been unauthorized activity involving the Check Deposit Services, tell us immediately by contacting us as specified above and promptly change your password.

6.2.13 Check Deposit Services Disruption

The Check Deposit Services might not be available from time to time due to maintenance, technical problems or other reasons. We are not responsible if the Check Deposit Services are not available. We cannot assume responsibility for any technical or other difficulties or any resulting damages that you may incur. We reserve the right to change, suspend, discontinue, or limit your use of the Check Deposit Services, in whole or in part, immediately and at any time without prior notice to you.

6.2.14 Ownership and License

You agree that we and our service providers, as applicable, retain all ownership and proprietary rights in the Check Deposit Services, associated content, technology, and website(s). Your use of the Check Deposit Services is subject to and conditioned upon your complete compliance with this Agreement. Without limiting the effect of the foregoing, any breach of this Agreement immediately terminates your right to use the Check Deposit Services. Without limiting the restriction of the foregoing, you may not use the Check Deposit Services:

● in any anti-competitive manner;

● for any purpose which would be contrary to our business interests (as deemed by us in our sole discretion); or

● to our actual or potential economic disadvantage in any aspect.

You may not copy, reproduce, distribute or create derivative works from the content and agree not to reverse engineer or reverse compile any of the technology used to provide the Check Deposit Services.

6.2.15 Indemnification and Limitation of Liability